Just $225M in 2015, sales of SD-WAN gear will hit $1.19 billion this year as enterprises pick it to resolve challenges created by increasing cloud, mobile, big data and analytics traffic

As network pros rely more and more on SD-WAN to streamline connections among enterprise sites, the market for this technology will balloon from $225 million in 2015 to $1.19 billion by the end of this year, according to IDC.

Over the next five years, SD-WAN sales will grow at a 69% compound annual growth rate, hitting $8.05 billion in 2021, according to IDC’s Worldwide SD-WAN Forecast, 2017–2021.

As businesses adopt what IDC calls “third-platform” technologies such as cloud, mobile, big data and analytics, they put increased strain on the network. As organizations look to better connect their remote and branch office employees and provide them better quality network services, SD-WAN will continue to grow.

A 2016 survey of enterprise communications professionals found that 30% of respondents plan to migrate to SD-WAN within one to two years.

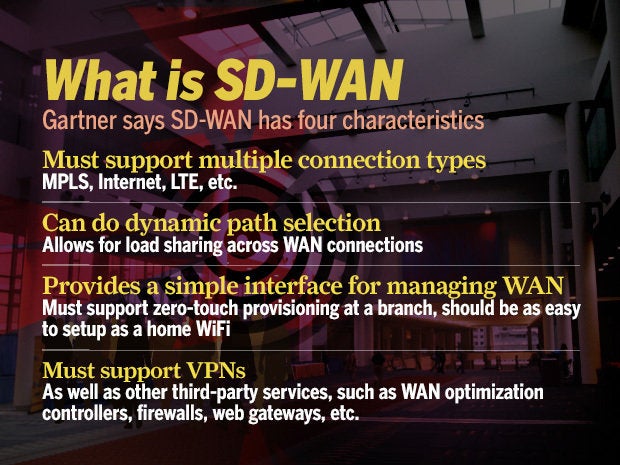

+MORE AT NETWORK WORLD: SD-WAN: What it is and why you’ll use it one day +

Gartner

Gartner“SD-WAN offers compelling value for its ability to defray MPLS costs, simplify and automate WAN operations, improve application traffic management, and dynamically deliver on the cost and efficiency benefits associated with intelligent path selection,” IDC analysts Rohit Mehra and Brad Casemore write in the report.

Any business that’s significantly using SaaS applications (like Office 365 or Salesforce.com) or Unified Communications (UC) services, has a substantial number of branch office locations or a large number of mobile workers could be a candidate for SD-WAN to improve network connectivity back to the campus and to cloud-based applications. “SD-WAN provides the complementary capstone for hybrid cloud application delivery,” Mehra says.

SD-WAN offerings typically include a bundle of routing and WAN optimization infrastructure combined with policy controller and overlay network software, which enable applications to customize the network characteristics they need. For example, an SD-WAN could ensure that an MPLS virtual private network (VPN) or UC services always have first priority for network connectivity, while giving secondary priority for high-bandwidth traffic like video and social media.

Software defined networking (SDN) has become an invaluable tool for creating more agile data centers, but applying SDN to the WAN has seen a slower uptake. Enterprises have often relied on a precursor to SD-WAN known as hybrid WAN. That’s the aggregation of multiple different types of network connections – MPLS, broadband, 3G/4G – to serve branch offices. SD-WAN takes that concept a step further by incorporating a centralized application policy controller, a software overlay and analytics features.

Providers like VeloCloud, Viptela, CloudGenix, Cybera, Versa, and Talari are some of the venture-backed startups in the SD-WAN market. There are also hosted SD-WAN offerings from communication service providers (CSPs) and cloud providers. IDC predicts CSPs will continue to launch SD-WAN services atop their existing MPLS offerings. Cable providers like Comcast Business and Charter are also likely to offer managed SD-WAN as an alternative to MPLS.

Router vendors, such as Cisco Systems and Nuage and established players in WAN optimization such as Riverbed Technology, Silver Peak and Citrix will all play in this market.